The Alabama Public Service Commission promulgated the regulations in a Final Order last December, but had stayed implementation while two of the companies, Securus and Global Tel*Link, challenged the new rates in court. But as the companies pursued protracted litigation, the Commission reasoned that it could no longer hold off on ensuring reasonable phone rates for residents who needed to talk to their incarcerated loved ones:

“The Commission has a duty to ensure that rates and charges are reasonable and just to both the ICS providers and the customers. During the course of these proceedings, the Commission has found that customers are paying too much for ICS. A continued postponement in implementation of the Final Order’s prescribed rates and ancillary fees would further delay the rate relief to ICS customers in Alabama.”

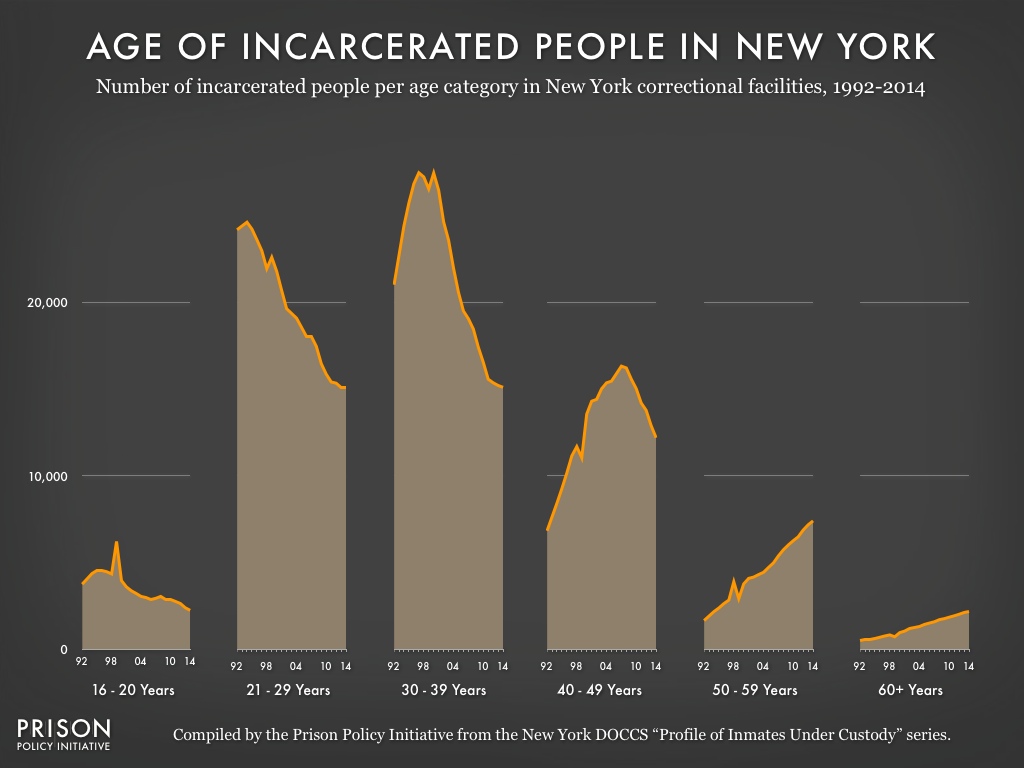

The rapid decline of all age groups under 50 years old and the rapid increase in people over 50 can be seen most clearly in this graph of the New York State prison population by age:

While the number of people behind bars has fallen for most age groups, the number of people over the age of 50 incarcerated in New York State prisons is climbing. (While we do not have an explanation for the bump up or down for each age group in 1999, we do not consider it to be significant given the clarity of the larger trend.)

While the number of people in prison under the age of 30 has been in almost constant decline since the mid 1990s, the number of incarcerated people in their 30s or 40s has been declining for about a decade. Throughout this period the number of people in prison aged 50 and older has been on a consistent and troubling rise.

There are only two possible explanations for this pattern:

The elderly could be on a crime wave, driving the increase in older people behind bars. (Not true, as we explain below.) Or,

Older people aren’t being released from prison.

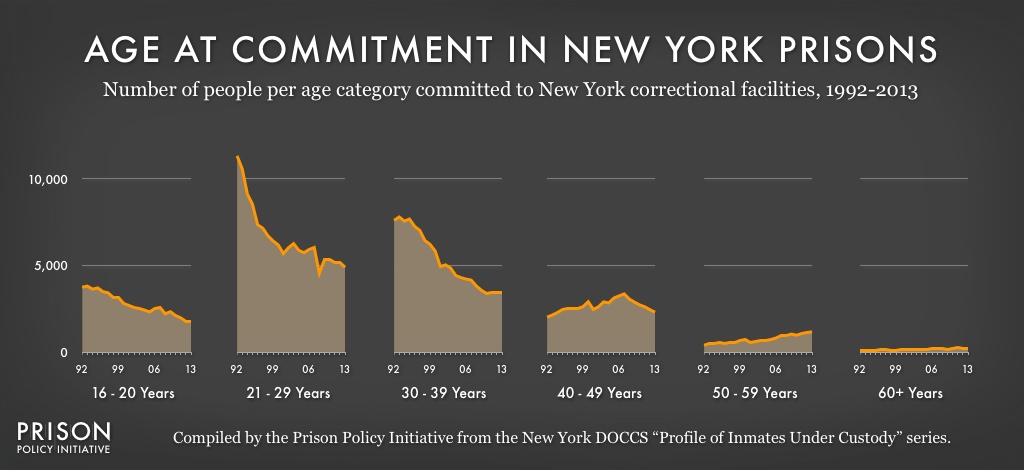

The first theory of an elderly crime wave is easily disproved by the graph below showing the age of people sent to New York State prisons each year:

The number of people sent to prison each year has been trending downward for all ages under 50 since at least 2007, and the number of people under age 40 sent to prison each year has been declining since the beginning of our data. To be sure, the number of people sent to prison in their 50s and 60s has been increasing, but the rate of growth is miniscule compared to the rapid growth seen in the incarcerated populations of these age groups in the previous graph.

The reason for this pattern unfortunately lies in the history of New York State’s sentencing laws and their current flawed parole practices. Many of the older people in prison have very long — but very old — sentences for violent offenses. And sadly, despite all of the other reforms, the parole board gives too much weight to the severity of the original offense, and too little weight to two key issues: people’s accomplishments while incarcerated and the low risks that elderly and infirm people pose to public safety.

Putting common sense back into parole decisions would be an excellent way to reduce the growing number of elderly people behind bars in New York State.

In general, Securus — a prison phone industry giant — is in a pretty profitable business. The company and its competitors vie for monopoly contracts to provide phone service in prisons and jails. Because the facilities demand a share of the proceeds, the incentive is to charge as much as the consumer — or regulators — can bear. But Securus exemplifies the industry’s obscene penchant for squeezing profits by fleecing their customers and shorting their business partners. As The Huffington Post wrote last week:

A presentation that the privately-held prison telecom company Securus made to investors that The Huffington Post obtained shows just how much money there is to be made as the state-sanctioned middleman between prisoners and the outside world: $404.6 million last year alone.

Securus, which provides phone services to 2,600 prisons and jails in 47 states, made $114.6 million in profit on that revenue in 2014. Securus’ gross profit margin — a measure of the difference between the cost to provide its services, and what it charges for them — was a whopping 51 percent.(*)

That’s not only unprecedented(**), it’s significantly higher than companies typically known for having high profit margins like Apple. And it’s certainly enough profit to buy up their rivals like JPay.

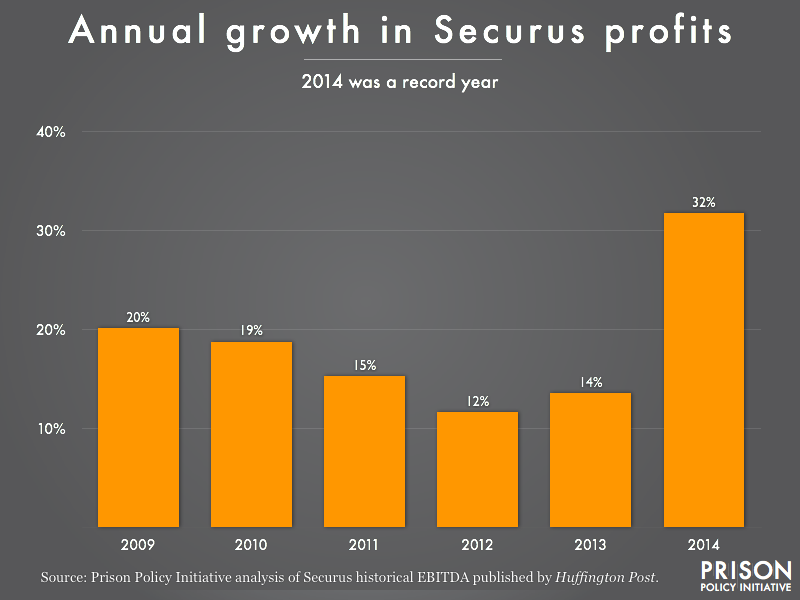

And these margins continue to grow. Our analysis of Securus’ profits from the investor slides reprinted by The Huffington Post shows the company’s profits took a huge leap upwards in 2014:

But what is driving these profits? Three shifts are likely behind Securus’ unprecedented profit growth:

Securus stopped paying commissions on interstate calls. The FCC issued an order capping the cost of these calls and prohibiting companies from treating the commissions as a legitimate cost of the call. Securus has, apparently, chosen not to share any portion of their profits with the facilities, keeping the profits all to themselves.

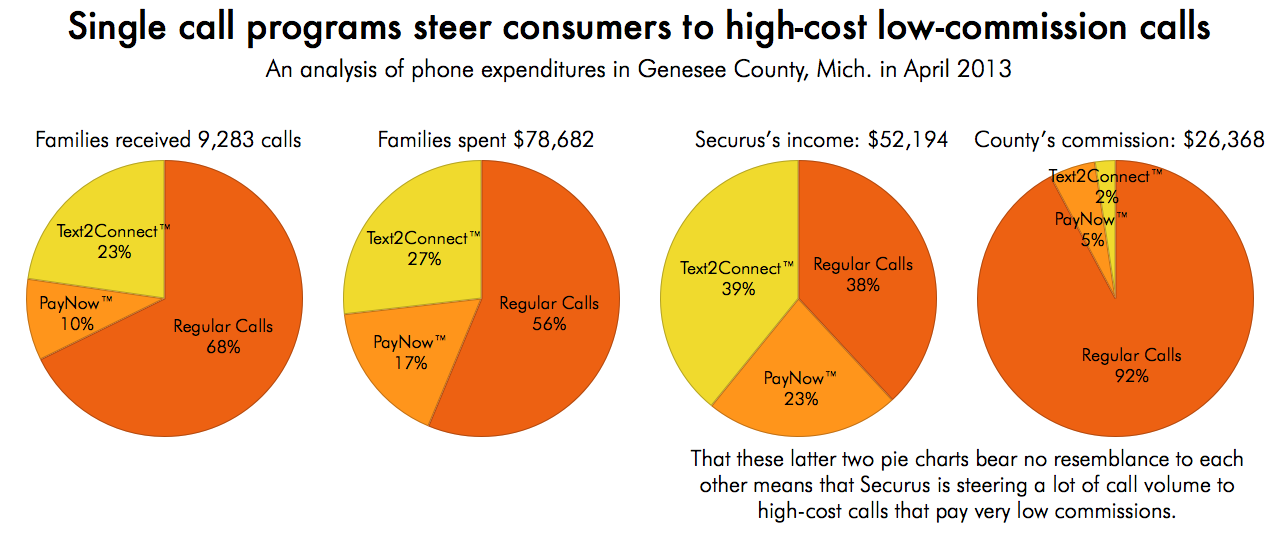

Securus is steering a greater portion of their call volume from regular calls to abusive “single call” programs that charge $9.99 via premium text message or $14.99 charged to a credit card for each call. As we explained in our January 2015 briefing, these calls are responsible for a disproportionate share of Securus’ profits:

These charts show four views of three types of calls in Genesee County, Michigan: by volume, by the cost to families, by where Securus makes its money and where the County earned its commission. (And as we explain in a footnote to yesterday’s article, just the credit card calls earn Securus $24-76 million a year.)

Securus has increased their typical(***) credit card deposit fee from $7.95 at the time of our report in May 2013 to $9.95 shortly thereafter. Since Securus disclosed that they charged credit card fees 4.8 million times in 2013, at $9.95 each in 2014, Securus revenue could be as much as $47 million from just credit card fees in their record profitable year.

As we explain in an article released yesterday, Securus’ business model is less about providing phone service than it is about harvesting fees. What this data shows is just how profitable that fee harvesting can be.

Notes:

(*) Securus challenges some of the numbers in the quoted Huffington Post paragraphs but Securus does not challenge the legitimacy of the investor slides published by Huffington Post.

(**) Because Securus is privately owned even seeing this data is unprecedented. The data on these slides shared with investors is also quite different from the story that CEO Rick Smith told the FCC last July (video at 208:45 seconds or transcript):

Page 198:

1 At some point in the presentation and

2 these discussions, I always get around to

3 discussing where I think we stand in terms of a

4 competitive company with competitive returns. And

5 I've heard three words during the session so far.

6 One is that rates are egregious. One is that

7 rates are abusive, and the other one is that rates

8 are predatory. I can look at our bottom line and

9 compare that to other companies' bottom lines.

10 Most of these companies you've heard of. And so a

11 few statistics before we can use any of those

12 words.

13 I looked at net income, kind of what you

14 can get from public statements, as a percentage of

15 profit. And here's the listing. Verizon was at

16 14.3 percent; not bad. Time Warner was at 11.4

17 percent, and I'm going in descending order now.

18 AT&T, we've all heard of AT&T and what they do,

19 they're at 10 percent. Century Link, think of that

20 as U.S. West Embark, Century, pretty big company.

21 I think the fourth largest local exchange carrier

22 in the United States; they're at 5 percent. And

---

Page 199:

1 now Securus brings up the rear at 1.4 percent. So

2 Verizon makes roughly 10 times what I make on a

3 comparable basis. Time Warner makes eight times

4 what I make. AT&T makes seven times what I make.

5 Century Link makes four times what I make. I'm

6 not saying that any of those are bad. I'm just

7 putting these things in the proper perspective in

8 terms of what we make bottom line after all of our

9 costs, and commissions does represent a

10 significant portion of our costs is a relatively

11 small number.

12 So we don't earn excessive profits. We

13 don't earn excessive profits. We don't earn

14 excessive profits. I said that three times for

15 the egregious and abusive and predatory kinds of

16 comments that come at us most of the time.

(***) The redacted data does not disclose Securus’ costs to process credit card transactions, but they must be below $9.95, both for the common sense reason that their competitors are able to charge less, and because some states like Alabama require Securus to charge less with no apparent ill effects. Securus reported 4,059,157 credit card transactions ranging from $5.00 to $6.95 in 2012. We calculate the average fee collected to be $6.82 and the median to be $6.95. For 2013, Securus reported 4,769,570 credit card transactions ranging from $3.00 to $9.95. We calculate the average fee collected to be $7.20 and the median to be $6.95.

Our analysis of the FCC’s Second Further Notice of Proposed Rule Making is that the agency is clearly onto the industry’s dirtiest trick: charging consumers hidden fees. Some of these companies call themselves phone companies, but the phone service is little more than a gimmick to charge fees.

We’re thrilled at the FCC’s attention to fees, but we haven’t yet gotten the media and lay audiences to understand that the distinction between rates and fees is far more important and far less semantic than it appears at first blush. Let me explain:

Rates: This is what you pay per minute, including any higher charge for the first minute of the call.

Fees: This is everything else you pay for “services” related to the call, including fees to open an account, have an account, fund an account, close an account, get a refund, receive a paper bill, or other charges that are made on a per-call basis, such as charges for “regulatory compliance” or “validation”.

The hidden fees can easily equal or surpass the base cost of a call. We estimate that families pay at least $386 million a year in charges like $9.50 for a credit card payment or $5 to receive a refund. On top of that, Securus and its competitors quietly pocket tens of millions of dollars tacking on an abusive $13.19 “single call” fee1 to 20 cent calls.

The fees are the direct result of the commission system (explained below) because they are a hidden revenue source that enables the phone companies to promise the facilities an otherwise unsustainable percentage of the call income.

Fees have become the new business model that the companies use to circumvent the FCC’s caps on the rates charged.

In sum, the fees allow the companies to both circumvent the FCC’s rate caps and make possible the entire shell game of winning contracts by promising to pay what are actually impossible commissions.

It’s easy enough to understand why high fees are bad for the families paying for the calls, but they are bad for the facilities too. As one of the more ethical phone companies recently explained in a colorful video, the companies are asked to compete on the basis of who will promise the facilities the largest share of the rate pie; but they are never asked to disclose the existence of an entirely separate pie of income extracted from the fees charged to the families. The companies playing the fee game look generous because they are promising to share up to 99% of the rate revenue with facilities, but that “generosity” is only possible because the company is hiding the revenue it collects from fees.

Sadly, some facilities learn about this and then look away. They don’t see a reason to stick up for their taxpayers, nor do they see any self-interest in enforcing ethical behavior with their business partners. This story illustrates what the facilities are missing:

Bonnie and Clyde rob banks and they agree to split the loot 50-50.

It turns out that Bonnie sometimes robs banks on her own without telling Clyde. He’s not going to care, right? As long as she doesn’t do something that gets them both caught, what impact does it have on him?

Well, one day, Clyde notices that they are making less money than they used to. The typical haul is down, but hey, it’s still easy money. But the strange thing is that Bonnie keeps on buying new cars and new clothes as if the hauls were huge like in the old days. Maybe Bonnie buys things on sale?

Clyde is getting suspicious, and nothing is adding up. It’s easy to trust Bonnie, and she is certainly being more helpful than ever. She’s always on time; heck, she volunteers to case the banks first and doesn’t ask for an extra share of the loot for her extra work.

Then one day, Clyde decides to get to the next bank even earlier to watch Bonnie case the joint. What does he see?

Bonnie isn’t casing the bank – she’s robbing it first.

We made it easy for sheriffs who want to protect their taxpayers and themselves from their partners. All they have to do is ask their vendors these easy questions about how fees and commissions are calculated.

What the sheriffs are missing is that by allowing their partners to fleece families out of half a billion dollars a year in fees, they are ensuring that the poorest families in their counties won’t have very much money left to pay for the actual, commission-producing, calls.

And phones aren’t the only industry in which fee harvesting is the new business model. Take our work on release cards. Private companies reach out to jails with offers to take over all of their money management woes – at no cost to the county.. Previously, jails had to keep track of the money people were arrested with or were sent by family members and then, upon release, issue a check or give cash. Now, private companies take the cash and give people pre-paid Mastercards instead. The jails ask: What could be more convenient than that?

The better question is this: How is it even possible to provide a valuable service for free? It’s not. These companies exist by charging the people who are forced to use their cards exploitative fees like $3.50 a week for the account, $0.95 for purchases, $3.95 for checking their balance, and $30 for closing their account.

Most people who run correctional facilities see it as their job to make our communities safer and stronger. One of the simplest ways they can meet that goal would be to start working much harder to ensure that the facilities aren’t complicit in making the poorest among us any poorer.

Focusing on fees is one of the most important ways to ensure that both families and facilities are protected from the companies that have the interests of neither at heart.

Illustrations by Prison Policy Initiative Research Associate Elydah Joyce. To help other organizations explain fee harvesting in their own work, she has made these illustrations available under a Creative Commons license on Flickr.

Footnotes

Single call programs are ostensibly designed for people who don’t want to set up accounts, but as we explain in a letter to the FCC, these programs are simultaneously the most expensive way possible for a family member to pay for a call and the least lucrative way for the facility to make any income. These programs go by a lot of names, but they typically charge families $14.99 for a single call if prepaid via credit card and $9.99 if paid via premium text message. In our letter to the FCC, we explain that in the case of Securus’ PayNow credit card program, it is possible to disaggregate the charges: a $1.80 call charge (with $1.60 going to the facility and $0.20 for the actual call) and a fee of $13.19. To be clear: Securus is charging a $13.19 fee for a phone call whose real cost is apparently only 20 cents. Based on the size of Securus’ business and data on how often PayNow is used in jails, we estimate that Securus makes between $24 million and $76 million a year in fees for their PayNow credit card product in jails. That calculation does not include their contracts in state prisons, their $9.99 Text2Collect product, nor the similar products of any of their competitors. ↩

One of the worst ideas to come out of the War on Drugs is sentencing enhancement zones. These laws mandate a higher penalty for crimes committed within a certain distance of schools. The intent is noble, but at huge distances like 1,500 feet, the laws are actually harmful.

Alternative Spring Break participant Arielle Sharma, research associate Elydah Joyce, and programmer Jacob Mitchell put together the illustration below to show just how far 1,500 feet really is. Just click on the image to understand why school zones fail to keep children safe. And check out our zones page for updates on the pending Connecticut bill that would roll back these zones, our reports on zones in Connecticut and Massachusetts, and our zones video.

To embed this animation on your own website, use this code:

Nils Christie, the world-renowned criminologist, a member of the Prison Policy Initiative advisory board, and one of my personal inspirations, passed away on May 27 at the age of 87.

I’m saddened to report that Nils Christie, the world-renowned criminologist, a member of the Prison Policy Initiative advisory board, and one of my personal inspirations, passed away on May 27 at the age of 87.

Christie came to my attention in 2001 when I tripped over a reference to his provocatively titled Crime Control as Industry: Towards Gulags, Western Style. The book reframed how I thought about both prisons and the movement to end them.

Even the title provided a completely new way to look at the problem. Rather than a “prison industrial complex”, which evokes an Eisenhower-era critique but little in the way of an organizing strategy, the framework of an industry seemed spot on:

Only rarely will those working in or for any industry say that now, just now, the size is about right. Now we are big enough, we are well established, we do not want any further growth. An urge for expansion is built into industrial thinking, if for no other reason than to forestall being swallowed up by competitors. The crime control industry is no exception. But this is an industry with particular advantages, providing weapons for what is often seen as a permanent war against crime. The crime control industry is like rabbits in Australia or wild mink in Norway–there are so few natural enemies around.

Christie later told me that he considered the book “sad”, and I tried to explain why, as someone living in the nation with the highest incarceration rate in the world, the book was liberating: You simply can’t change what you don’t understand; and like the light at the end of the tunnel, Crime Control as Industry provided both hope and a path.

Last night, comedian John Oliver did a great segment last night on bail (NSFW):

And on that topic, don’t miss Daniel Kopf’s article from two weeks ago on Priceonomics: America’s Peculiar Bail System. (Dan is a member of our Young Professionals Network. Stay tuned for the results of his research collaborations with us.)

And on Friday, Sally Herships on Marketplace did a great piece on the role, number and challenges of private police in the U.S. (Spoiler: There are more private police in the U.S. than public police, which raises troubling questions about who benefits when most policing isn’t in the public interest. Her story starts 13 minutes in.)